OSM Industry Intel • Spring 2026

The Phospholipid Shift: Why Your Liposomal “Carrier” Is Now Your Second Active Ingredient

New market data shows phosphatidylcholine is being repositioned from delivery material to functional co-active. Here is what that means for pricing, positioning, and your next product label.

If you manufacture or sell a liposomal supplement, you are already buying phospholipids. Phosphatidylcholine (PC) from sunflower or soy lecithin forms the structural shell of every liposome in your product. It is on your bill of materials. It is in your cost of goods. And until very recently, most brands treated it as exactly that: a cost. The price of building a better delivery vehicle.

That thinking is outdated.

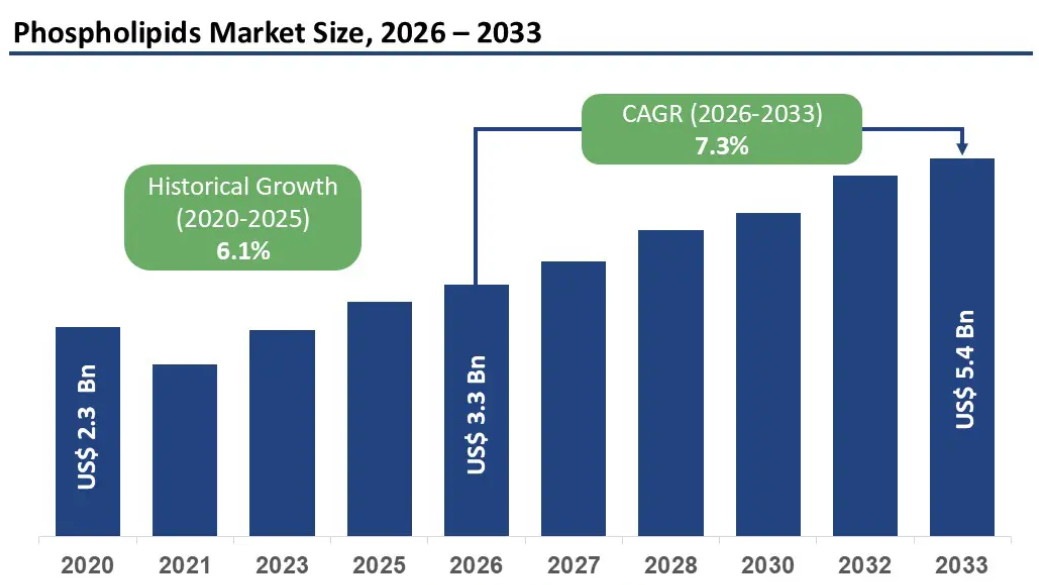

New market analysis from Persistence Market Research projects the global phospholipids market at $3.3 billion in 2026, growing at a 7.3% CAGR through 2033. But the number that should catch your attention is this: 45% of liposomal supplement revenue in 2026 is coming from products that explicitly list the phospholipid carrier as a functional ingredient for liver support, cognitive health, or both. The phospholipid is no longer just the shell. It is the second active ingredient on the label.

This represents a fundamental shift in how liposomal products are positioned and priced. And for brands working with a contract manufacturer to develop liposomal gummies, tinctures, beverages, or topicals, this shift creates an immediate opportunity to reframe an existing line item as a value-added selling point.

As we covered in our complete guide to liposomal supplement technology, the phospholipid bilayer is what makes liposomal delivery work. But the science behind phosphatidylcholine as a standalone health ingredient has been building for years. The market is finally catching up.

Phosphatidylcholine Is a Functional Ingredient, Not Just a Delivery Cost

Phosphatidylcholine is the most abundant phospholipid in human cell membranes. It plays a structural role in every cell in the body, but its functional relevance is concentrated in two areas that happen to be among the largest and fastest-growing supplement categories: liver health and cognitive function.

Liver support. PC is a primary component of bile and plays a direct role in fat metabolism and liver cell membrane integrity. Supplemental PC has been studied for its role in supporting hepatic function, particularly in contexts where the liver is under metabolic stress. This is well-established science, and it translates cleanly into structure/function claims that consumers understand.

Cognitive health. PC serves as a precursor to acetylcholine, a neurotransmitter involved in memory, focus, and cognitive processing. The FDA has issued a qualified health claim for phosphatidylserine (a related phospholipid) and cognitive function, and the broader phospholipid family is increasingly positioned in the brain health supplement category. The Persistence Market Research data shows phosphatidylserine growing at 8.2% CAGR, the fastest of any phospholipid product type, driven specifically by consumer willingness to pay for clinically validated brain health ingredients.

The sourcing shift matters too. Sunflower-derived phospholipids are growing at 8.4% CAGR, the fastest source-level growth rate in the market. The driver is straightforward: sunflower lecithin is non-GMO and allergen-free, which removes two of the most common label objections in premium supplement retail. Soy-derived phospholipids still hold over 55% market share, but that dominance is eroding in clean-label channels. Brands using sunflower-derived phospholipids in their liposomal formulations can market that sourcing decision as a quality differentiator on the label.

The math on “2-in-1” positioning:

A standard liposomal vitamin C tincture already contains a meaningful dose of phosphatidylcholine as the liposomal carrier. That PC content has functional relevance for liver support and serves as an acetylcholine precursor.

A brand currently marketing “Liposomal Vitamin C for Immune Support” can reposition the same product as “Liposomal Vitamin C with Essential Phospholipids: Immune Support + Liver and Brain Health.” Same formulation. Same cost of goods. Meaningfully stronger value proposition.

That repositioning justifies the premium price point of liposomal formats over standard capsules and gives consumers a concrete reason to choose the liposomal version beyond “better absorption.”

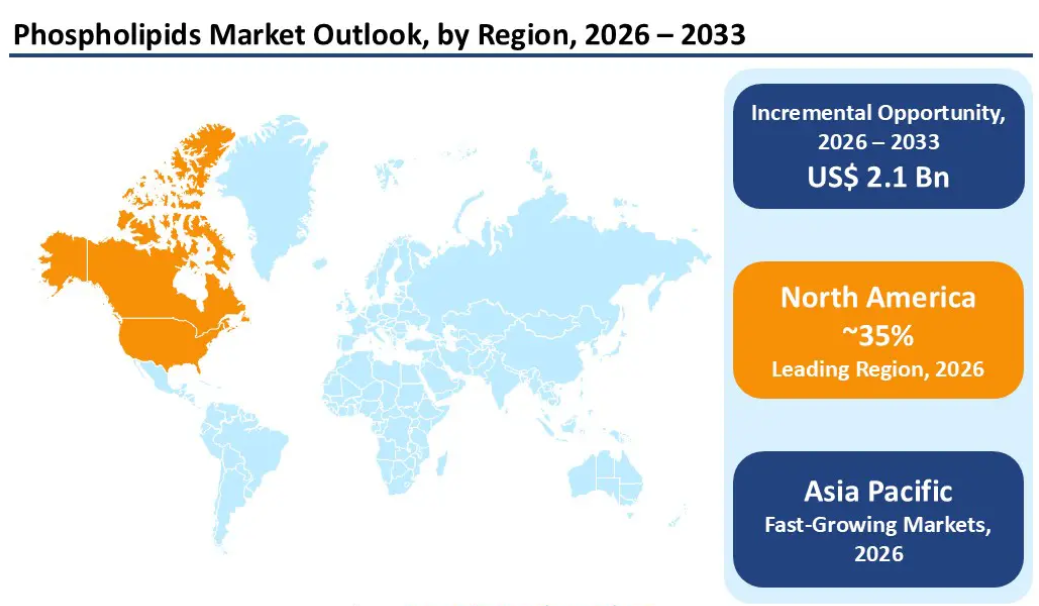

The nutraceutical supplement segment commands over 38% of the phospholipids market by end-use, the largest single category. North America holds over 35% of global phospholipid revenue (roughly $1.15 billion in 2026), driven by FDA regulatory infrastructure, pharmaceutical R&D demand, and established supplement industry procurement channels. The regulatory environment is favorable: lecithin is listed under 21 CFR § 184.1400 as GRAS with no limitation beyond good manufacturing practice.

In practical terms, this means the raw material your liposomal products already contain has a well-characterized safety profile, clear regulatory status, and growing consumer demand as a standalone functional ingredient. The opportunity is in recognizing that and putting it on the label.

How to Build the “2-in-1” Phospholipid Story Into Your Product Line

The practical application here is straightforward, and the best part is that it works across every liposomal format. If your product already uses phospholipid encapsulation, you already have the ingredient. The work is in the positioning, the labeling, and (in some cases) optimizing the phospholipid loading to support the dual-benefit claim.

Liposomal tinctures with phospholipid callouts. Liquid tinctures are the natural format for this strategy because the phospholipid content is typically highest per serving. A liposomal vitamin C, glutathione, or B-complex tincture can prominently feature “with Sunflower Phosphatidylcholine” on the front label and include liver and cognitive support language in the structure/function claims. The creamy texture that comes from real phospholipid content becomes an authenticity signal that reinforces the premium positioning. Consumers are increasingly aware that thin, watery “liposomal” liquids probably contain minimal phospholipids, so the texture itself becomes a trust marker.

Liposomal gummies with dual-benefit positioning. The gummy format continues to lead supplement adoption, and liposomal gummies are an emerging category where the 2-in-1 story is particularly strong. A liposomal CoQ10 gummy positioned as “Heart Health + Essential Phospholipids for Cognitive Support” tells a more complete health story than CoQ10 alone. A liposomal curcumin gummy can add “with Phospholipids for Liver Support” to create a multi-pathway anti-inflammatory product. The phospholipid content that makes the liposome work also makes the product label more compelling.

Recovery beverages with phospholipid branding. The functional beverage market is one of the fastest-growing supplement categories, and ready-to-drink products have a unique opportunity to tell the phospholipid story on the can or bottle. A recovery beverage with liposomal B vitamins for muscle repair, electrolytes, and a callout for sunflower phospholipids creates a product with three distinct functional pillars instead of one. That kind of multi-benefit positioning performs well in retail environments where products have seconds to communicate value.

Topical products with phospholipid skin benefits. The phospholipid story extends to topicals as well. Phospholipids are naturally skin-conditioning because they integrate with cellular membranes on contact. A recovery topical or skin wellness cream that features liposomal delivery of curcumin or hemp extract can also highlight the phospholipid content as beneficial for skin barrier function. That turns the delivery system into a third functional claim alongside the primary active and the recovery benefit.

Pricing and Positioning Implications

The phospholipids market data tells a clear story about where consumer spending is headed. The nutraceutical segment commands the highest ingredient value-add in the market. Phosphatidylserine and phosphatidylcholine in branded supplements generate disproportionate downstream revenue compared to the same phospholipids used as commodity emulsifiers. The difference is positioning.

Brands that treat their liposomal phospholipid content as a delivery expense are leaving margin on the table. Brands that position the same content as a functional co-active with its own health benefits can justify a higher retail price, tell a richer product story, and differentiate from the growing number of “liposomal” products flooding the market with minimal actual phospholipid content.

As AI-driven discovery platforms reshape how consumers find supplements, products with multiple verifiable functional claims and transparent ingredient sourcing will surface more frequently than single-benefit products with generic labels. The phospholipid co-active strategy positions your product to win in that environment.

The ingredient is already in your formula. The market data supports the positioning. The regulatory framework allows it. The question is whether your label reflects the full value of what your product contains.

Ready to Optimize Your Liposomal Product Positioning?

OSM formulates liposomal gummies, tinctures, beverages, and topicals with sunflower and soy phospholipid options, low MOQs, and full turnkey services from our USDA Organic certified, GMP facility. Let’s talk about building the 2-in-1 story into your next SKU.

Start a ConversationSource: Persistence Market Research. “Phospholipids Market Size and Trends Analysis.” April 2026. Global market projected at US$ 3.3 billion (2026) growing to US$ 5.4 billion by 2033 at 7.3% CAGR.

This article is for informational purposes only and does not constitute medical or regulatory advice. Supplement brands should consult qualified counsel regarding product claims, labeling, and compliance. Organic Supplement Manufacturing (OSM) is a contract manufacturer of dietary supplements, gummies, tinctures, beverages, and topicals operating from a USDA Organic certified, FDA-registered, third-party GMP certified facility in Plain, Wisconsin.